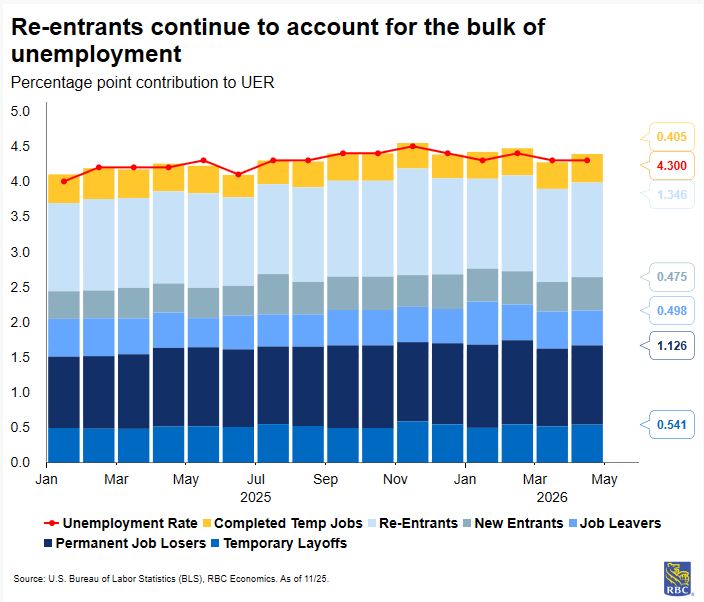

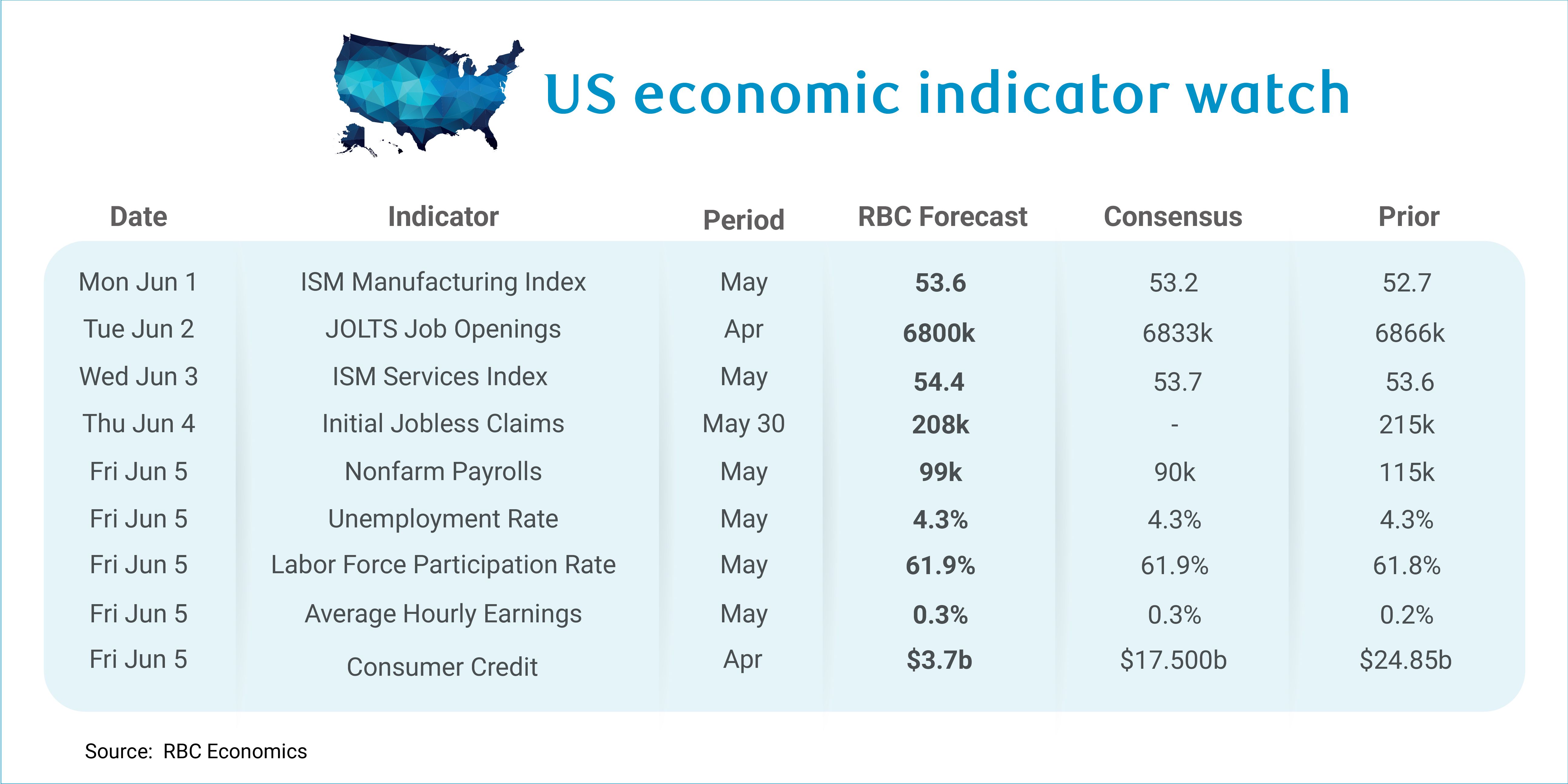

Next week, the May employment report will be front-and-center. We expect 99K jobs were added to payrolls with the unemployment rate holding steady at 4.3%. So far in 2026, the labor market appears to be on solid footing. Still, on aggregate, new job creation has been quite limited with monthly payroll gains averaging 55K over the past six months. But the interpretation of payroll gains is changing.

Our estimate of breakeven employment remains exceptionally low, as retirements create openings that when backfilled, don’t show up as payroll gains. Coupled with the precipitous fall in immigration, the labor market needs far fewer new jobs for the unemployment rate to hold steady. In this lens, we expect the Fed will rely more on the unemployment rate than the payroll report to gauge labor market health.

A key risk remains coincident oil and tariff shocks: if firms cannot pass on higher input costs, margin compression could translate to headcount reductions. By our calculation, the US economy would need to shed 1 million jobs by year-end for the unemployment rate to rise sufficiently to trigger the Sahm rule. This would require all sectors to respond to higher costs with layoffs rather than price increases – and for now that is not playing out. PPI has re-accelerated dramatically in 2026, confirming that passthrough is happening. Limited layoffs, as evidenced by stable jobless claims data, have helped keep the unemployment rate from rising. Still, the unemployment rate is rising for some groups – most notably recent graduates who are facing competition from AI.

What Else to Watch Next Week

- We anticipate the JOLTS data will show a slight decline in job openings for April (to 6800K). Indeed Hiring Lab’s job postings index fell 1.2ppts in April, suggesting the headline number will be little changed.

- We get both ISM Services and Manufacturing indexes for May, and both are expected to come in higher than last month. But the headline strength will likely be overshadowed by the price indices which are likely to show continued input pressures rising as energy costs remain elevated.

- For ISM Services, we expect headline will report 54.4. The Fed regional services survey showed Kansas City and Richmond in expansion, Texas contracting to a lesser extent, and only Philly Fed deteriorating.

- Initial jobless claims are expected to come in at 208k for the week ending May 30th. Initial claims have largely been rangebound since mid-February (from 200k to 220k) as firms avoid layoffs.

- Consumer credit likely increased by $3.7B in April as households continue to rely on credit to buffer higher gasoline spending. That said, consumers have largely leaned on savings so far—the personal savings rate has fallen from 4.5% to 2.6% between January and April – suggesting credit hasn’t yet become the primary release valve.

Comments

Join Our Community

Sign up to share your thoughts, engage with others, and become part of our growing community.

No comments yet

Be the first to share your thoughts and start the conversation!